Bostoncoin update Jan-Feb 2024

The USA ain’t A-OK, but RUOK?

“Everyone has a plan until they get punched in the mouth.” Mike Tyson’s words echo those of fellow warriors Dwight D. Eisenhower, Napoleon, Prussian General Helmuth Von Moltke and allegedly go back as far as ancient China. It is claimed that Sun Tzu said “no plan survives first contact with the enemy”.

We would all like to think we have a plan for life, but then someone or something hits, and the plans go out the window as we struggle to react and survive. If you get hit five or six times in a row, it’s possible your plan-making skills are no longer viable as you are no longer thinking clearly.

Some people will recall that the events of the 2008 Global Financial Crisis (GFC1) caught 99.99% of Wall Street investors off guard*.

The US Federal Reserve could not wind back the clock and stop rogue banks from giving NINJA** loans to the unemployed. Instead, the Fed listened to the morally and fiscally bankrupt rogue banksters who begged the government for unlimited cash-printing.

Quantitative easing (“QE”), financial stimulus or fecklessly trying to dig yourself out of a hole; call it what you will, it does not end well.

Printing extra currency means there is more cash in the system, but the same amount of goods. Inevitably, prices go up as the dollar’s value goes down. The official inflation rate puts the blame on businesses or sellers for “putting prices up”, but the real culprit is the banksters printing too much cash and devaluing your dollars.

Immediately after the 2008 GFC1, the official inflation rate was around 8% (reportedly much higher on the streets), and the poor people had to get used to being at least 10% poorer.

Just as reparations after World War One sowed seeds in Germany for an all but inevitable WW2, the Fed’s reactions to GFC1 sowed the seeds of what came next. Overzealous cash printing after 2008 contributed to the debt-ceiling crisis of 2010 and the US government shutdown in 2012.

*not everyone was unprepared. Michael “the Big Short” Burry knew what would occur in 2008. He bet against the banks and made a billion dollars. Jeremy “the big dufus” Britton wrote a book in 2006 to warn everyone about the 2008 GFC. He made a few thousand people very wealthy, but did not make a billion dollars.

**NINJA loans: an acronym meaning the borrower has No Income, No Job or Assets. Rogue banks gave out NINJA loans to people who could not pay them back, and caused the debacle known as GFC1. Fed intervention stopped six years later, but the taxpayer is still on the hook.

Math for the masses: you’re being √∞

Prior to GFC1, the US M2 cash supply was around $7 trillion, and afterwards, it was around $10 trillion. Politicians and billionaires who had their funds invested into stocks, bonds and property, with almost nothing in cash, celebrated the fact that they had managed to (allegedly) stop the (allegedly) worst financial depression in history by printing a boatload of cash for the masses. The masses, who had most of their funds in cash that had just been devalued by 30 to 50%, may not have been so jubilant.

The average person on the street does not really see the devaluation of their dollars; they mostly notice the rising price of goods and services. Instead of blaming the Fed and the banksters, the shafted people often ignorantly blame the politicians. One alleged leader is voted out, and another puppet leader is voted in, with no acknowledgement that the true controllers of a nation are the ones who print the currency.

The fiat printing press and QE programs started in 2008 and did not stop until 2014… Yes, the cure was arguably worse than the disease.

Fast forward a little: the economy that has not yet recovered from the hangover caused by its reckless lending is hit by another uppercut. The 2020 pandemic strikes, and we are now in GFC2. Once again, the Fed reacts by printing cash like there are no consequences.

During the pandemic, the US M2 cash supply increased from $15 trillion to around $22 trillion, a 46% increase in less than three years. For those playing at home, the US government’s “official” inflation figures in those three years were 7%, 6.5% and 3.5%, respectively (a total of 17%).

If you think that increasing the cash supply by 46% only adds 17% inflation, then you cannot legally be a math teacher, but you may be able to get a job in politics.

The Fed giveth, and the facts taketh away

Someone who may not get a job in politics, due in part to him being almost too honest, is current US Fed chair Jerome Powell. In an interview with 60 Minutes, Powell stated, “…the U.S. federal government is on an unsustainable fiscal path. … the debt is growing faster than the economy…”

US debt is now around $34 trillion, and grew around 3% in the last month. The US GDP or income is “officially” 3% per year.

Take a deep breath. Imagine your cousin runs a company, and wants you to invest in the business. They show you the books: profits are growing by 3% per year, and debt is increasing by 3% per month. How much stock would you buy?

Take another deep breath. Imagine you’re an employee. You work hard and get the occasional raise or promotion. Your take-home pay increases by 3% per year to keep up with “official” inflation, but your debt increases by 3% per month, more than ten times as fast. On a scale of Keith Richards’ liver to Hotel Hiroshima, how ruined are you?

Douglas Adams says, “Don’t Panic”

Despite the gloomy imaginings above, things can still turn out OK… for you, at least. The fact is, unless you’re ridiculously incompetent at math and finances, you are not, at this moment, increasing your debt ten times as fast as you make money. You will probably be OK.

Sure, the US economy is circling the drain, and the Rule of 72 dictates that there will probably be another government shutdown, another debt ceiling crisis, and possibly another Moody’s downgrade of the USA from AAA to A-, likely inside of 24-36 months, but that’s OK, because it’s just the US economy failing and not you personally.

You cannot control the entirety of a dying empire, but you can control where you put your own funds in the here and now.

As central banks print more devaluing cash to the point of worthless wallpaper, you can take control of your finances by investing in something that cannot be minted, printed or devalued.

Several years ago, in September 2019, six months before the COVID19 pandemic lockdowns, we warned readers about a possible stock market crash and ensuing currency debasement (because apparently, printing cash is all the Fed knows how to do in a crisis).

Back in those halcyon pre-pandemic days, we suggested that gold, silver and *some* (not all) cryptocurrencies could be a safer place to put your funds. It was a bold call, but it paid off.

Within a few months of our forecast, stocks tumbled, the Fed printed, cash crashed, and, amongst the melee, gold increased 50%, silver prices rose 100%, and Bitcoin rose over 400%. You’re welcome

If you were not around in 2019, or not reading this column, that’s OK. You still have plenty of time to act before the next wave of what we will be calling GFC3.

Because the Fed can print cash faster than you can save it, and because the Fed increasing M2 cash supply mostly hurts those who save in cash, the idea would be to hold very little in cash; only as much as you really need to pay your bills. To beat the Fed, you could invest as much as you can into growth assets, whilst remaining mindful of your risk profile.

In tumultuous times, when the price of goods can increase by more than 15% per year, you need to be invested in something going up by at least 16%. That 16% is assuming you pay no taxes. If you are paying normal taxes, your investment may need to return closer to 20% or 30% to beat inflation. Otherwise, you could be going backwards.

No, you do not run the Fed, but you do have the power to control the destination of your dollars. Choose wisely, and take action, because whether you strike, block, duck or dodge, anything is better than standing still and waiting to get hit again.

How did we do this month?

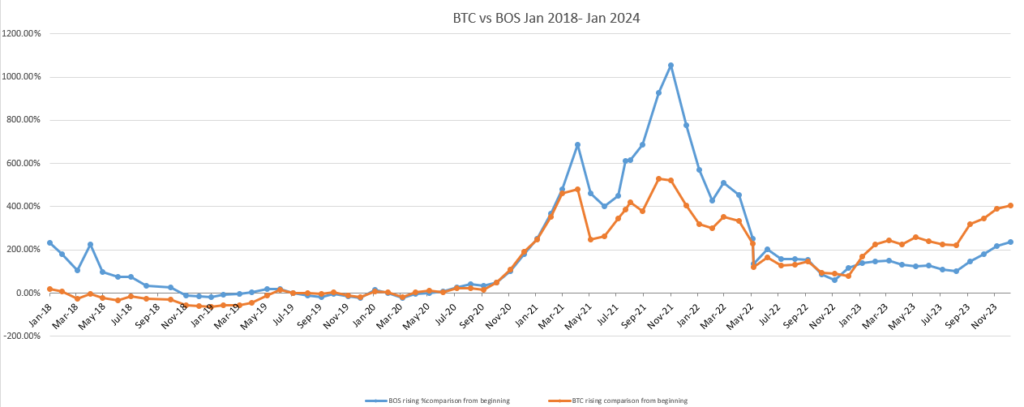

Bostoncoin

A few standouts:

Solana up 413%

DexCheck up 229%

ChainLink up 256%

Jan 30

BOS Price AUD 101.0850541048

BOS Price USD 66.5033238553

This is a 55% increase in one year for the Bostoncoin Fund.

That’s a lot more than inflation or bank interest. Check with your friends to see what their investments made in the past year. Perhaps share our number with them if it is less than 15%. You may turn your casual friend into your very best friend, and we may even send you some cool Bostoncoin swag to say thanks.

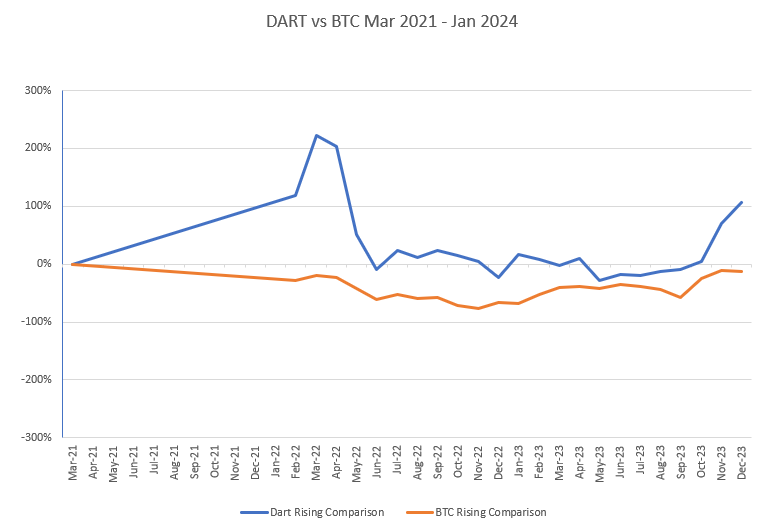

DARTcoin

Some nice gains from

ThorChain up 264%

Render up 323%

TRX up 180%

Jan 30 2024

DART Price AUD 190.6187607007

DART Price USD 125.4721458181

As we learned in 2022, this little puppy can seriously outrun during altcoin season, so hang onto your hat!

CAUTION: Investing into growth assets can make you large gains, but can also bring losses. Growth investments can grow up as well as down. Understand your risk profile, diversify amongst different asset classes and seek the assistance of a trained financial professional, preferably one who knows their way around stocks, bonds, property, precious metals, commodities and crypto.

Feel free to get in contact with our office to ask any questions. There are no silly questions, and it’s silly to *not* ask questions about this new asset class.

Stay safe, stay educated and we will see you next month.

JB