#BostonCoin *pup*date, Sept-Oct 2019

Remember: the world of crypto exists inside the world of global finance

It has been an interesting month in Cryptopia, as we feel the effects of what is happening in the outside world, as well as in our own little corner of the globe.

Bitcoin prices dropped hard in September, possibly due to price manipulation by nasty Bulls*, and then reached a new floor before starting a climb again. It is interesting to see the new higher floor around US$8000, a significant increase from the previous floor of around US$3000 earlier in 2019.

After hitting US$19 000 just before Christmas 2017, bitcoin dropped to around $6000 by Feb 2018. We then tested $11k, back to $6k in April 2018, up again in May and then back to $6k in July. With a few sparse spikes, bitcoin sat around $6k for the rest of 2018… right up until that week before Christmas, when it plummeted to around US$3000.

Those who have been in crypto for a few years (or those who have been reading old #BostonCoin newsletters) will know that “baby” bitcoin has not been around long enough to have many traditions, but it does seem to have an annual pattern.

BTC: Back To Christmas

We have noticed the pattern, and you will too: Bitcoin tends to head south around Christmas and then rises again around Easter. This has happened almost every year since bitcoin started, and (aside from the halvening**) is the only long-term price trend we have seen so far. This annual pattern is less to do with any Christian festivities (or their pagan origins), and far more to do with Chinese New Year.

Asian investors who purchased BTC earlier in the year for a low price, and watched the price go up by sometimes 300% to 1000%, will sell down in December so they have money for the festive season in Asia. Chinese New Year is similar to Christmas, Thanksgiving and New Year’s Eve all rolled into one, and is a big deal in Asian countries. Most people will travel to be with family, and some businesses will close completely for up to two weeks.

This business downtime and family time obviously costs a lot of money, so Asian investors need to “cash in” towards the end of the year. Those in the west who watch bitcoin prices drop by 50% to 70% in December may feel terrified, but the wise investors #HODL fast and wait for the Easter emergence to repeat.

Dancing on the ceiling, falling to the floor, and magic*

As bitcoin tends to rise to new heights more often than annually, it can be tempting to “dance on the ceiling” during the highs. When crypto prices went 1000% bananas in 2017 we had an influx of generosity and people gifting crypto to friends and family (which was great to see). We also had an increase in theft, ransom demands, scams, greed, ponzi schemes and outright $100 000 Tamagotchi nonsense (does anyone want to buy my crypto kitties, anyone? Anyone?)

When crypto crashes to the floor, it can be a sobering event for many people. Fortunes can be lost, and some people may feel regret for investing on pure speculation, or purchasing silly things and bits of bling whilst they are feeling rich. The thing to remember is that there is a magic phrase which prevents bitcoin from going any lower. That magic phrase is not the levitation spell from Harry Potter (“wingardium leviosa”), the magical phrase is “the halvening”.

**The Halvening

Creator of bitcoin, Satoshi Nakamoto knew that computing power is always increasing. Whilst the first bitcoins were mined using $1800 1Gig laptops, Moore’s Law would suggest that anyone with a $99 smartphone could now be mining BTC more than twice as fast as a large 2009-spec computer.

Satoshi built into bitcoin a factor known as the ‘halvening’, which means that the number of bitcoin rewards for mining will halve every four years. This makes bitcoin harder and harder to mine, even as computer processing power increases.

As of late 2019, it takes around $3000 worth of electricity to mine a single bitcoin. This is not even counting the cost of internet access, nor the cost of the hardware required. This is an obvious indicator of why, when bitcoin crashed down from its $20k highs to its lowest lows, it never went below $3000.

Anyone who was mining bitcoin was not going to sell BTC for less than the bare cost of production; that would be crazy. Even if the price briefly nudged $2999, savvy investors would be stockpiling BTC at ‘below cost’ and drive the price back up again.

With the next halvening event scheduled around Easter 2020, the cost of mining a single bitcoin may exceed $6000, just in electricity costs. Without crystal balls, we cannot fathom the next bitcoin ceiling, but we are confident that the new floor will be $6000 for the next four years, and a minimum of $12 000 thereafter.

Bitcoin newbies may get caught up in the hype as they see the price increase by 300%, 500% or 1000% and media coverage increase. Newbies may buy in at a peak and then suffer on the way down. Veterans will know about the halvening, and the annual festive reckoning, and may fare a lot better over time.

Cryllionaires, *Bulls & Bears

It is important to remember that the crypto universe is a small subset which exists inside of the larger global financial world. Events which occur in the broader world can, and will, affect crypto prices (subject to psychological cost floors, as above).

Stock market pundits often speak of “bull” or “bear” markets, depending on price movements and overall sentiment. It’s easy to remember that a bull attacks by thrusting its horns upwards, and a bear attacks by thrashings its claws downwards. When the markets move up, bulls (or buyers) are said to be in control, when the market moves down, it is the domain of the bears (or sellers).

Occasionally we do see some nasty bulls who pretend to be bears, selling out for a loss in order to drive market sentiment down, and then buying up big at the bottom. It truly is a jungle out there, so be aware, and watch the broader markets, not just the crypto news.

What’s going on in the big bad world?

Negative interest means you pay the banks to hold your money

With several countries in zero or negative interest rate environments (Japan, Bulgaria, Cypress, Switzerland, Sweden), and several more countries likely to follow, this makes people seek deflationary assets, such as gold, silver and finite cryptocurrencies. Like gold and silver, bitcoin is finite in that there will only ever be 21 million coins. Supply is capped, so theoretically demand will always tend to increase.

(Fortunately, you don’t have to own an entire bitcoin, in the same way you don’t have to own an entire kilogram of gold: each asset is divisible so you can purchase $1 worth or $100 worth, and still benefit from the percentage price gains.)

Some cryptocurrencies are technically infinite, meaning the creators can make as many of them as they see fit, just like paper currency. Obvious examples are USDC, TrueUSD or Tether, which are linked to the $US, and supply must swell every time the Independent Federal Reserve turns on its magical printing press to turn a penny’s worth of paper into $100 note.

Other technically infinite cryptocurrencies include Ethereum, which has long been #2 to bitcoin’s #1 market cap. Being a potentially infinite supply does not make a cryptocurrency ‘better’ or ‘worse’, it is just ‘different’; in the same way that gold and silver are different to paper currency. You do not have to choose one or the other, you can always #haveboth.

Nobody is going to stop holding fiat cash and simply hoard 100% gold, as this would be unfeasible for daily occurrences such as buying groceries, sending money to friends or paying bills. Nobody who is holding a few bricks of gold or a few bitcoins would drop those and convert to 100% cash, for three reasons:

Gold and bitcoin are almost perfect hedges against inflation,

gold and bitcoin have outperformed stocks and property over the last 25 years, and

oh damn! It’s now illegal to hold too much cash

Two years in prison for using cash?

The recent “cash bans” which have been put into place in several countries also make crypto an attractive proposition. As at late 2019, Australia will imprison anyone who holds or uses over $10 000 in a cash transaction, so kiss goodbye to buying a second-hand car for cash, or selling your old collectables at a garage sale or market.

The government says this cash ban is to crack down on illegal activities such as tax evasion or selling drugs, however tax evasion and illegal drugs have been around for 100 years, and marijuana is being decriminalised all over the world, so we don’t believe that laughable explanation. What coincides with this cash ban is something with a very recent history: negative interest rates.

Germany has banned cash transactions of over €5,000. Italy, Spain and France claim to have banned transactions over €3,000. Sweden and the Netherlands are similar, with more EU countries expected to follow. Most of these countries have interest rates at record low levels. Israel, Australia, New Zealand, the UK, Canada and the USA have interest rates of 2% or less, with the Aussies predicted to hit 0.5% by the end of this year.

Interest rates which are negative (or below inflation rates) mean that you are paying the bank to hold your money. This plan is patently ridiculous and has never occurred before in human history. The whole idea of the bank is to pay you a premium for lending them money, with the premium being commensurate with the risk you take of not getting your money back. Smaller Building Societies and Credit Unions have always paid a slightly higher rate than the larger banks, as the deposits were seen as “safer with the bank”.

As we have seen in the 1930’s and as recently as the 2008 GFC, banks are never “too big to fail”, and investors can lose all their savings. You may be young enough to have not been alive during the Great Depression, you may be young enough to have been born after the Gold Standard was abandoned in 1971, but you probably do recall the 2008 GFC. Savings were wiped out, homes were lost and the banks had a big bail-out from a government who was already in unwieldy debt. This time the banks may not be so lucky.

The only lesson we learn from history is that we do not learn from history

In 1918, after the “Great War”, author H.G. Wells called the European conflict “the war to end all wars”. The phrase was echoed by US President Woodrow Wilson, who hoped that after such a devastating event, humans would realise the folly of war, and unite for peace and democracy. It seems that humans have a very short memory, and within a couple of decades, the world was at war again, in what was called “World War Two”.

It seems that society still has a form of collective amnesia, or politicians have an inability to deal with issues with any semblance of finality. Since the “war to end all wars” there have been many more wars in hundreds of locations, and even sequels, as we had WW1 and WW2, Gulf War 1 and Gulf War 2, and so on. We now look ready to be having déjà-vu again as the west stares down the barrel of #GFC2.

#GFC2

After the ridiculousness of the sub-prime mortgage fiasco and the credit scandals, the 2008 GFC was a foregone conclusion. Unscrupulous bankers had played nonsense games for too long, with too much risk and someone was bound to get hurt. Unfortunately, it was not the billionaire bankers, but ordinary mum-and-dad investors who paid the ultimate price.

To try to ‘save the banks’ who had no money, governments with already high debts borrowed fictitious money from the banks to give to the banks (yes, it really was that simple and that ridiculous). This was not a good move. Aside from the fact that billions of bailout dollars were wasted or embezzled, the government’s role would have been better as totally passive: let the bad banksters fall over and learn a valuable lesson, whilst the good bankers survive.

Instead, we find that a decade later, the banksters who were unpunished are up to their old tricks again (even after the Banking Royal Commission), and this time, the governments are too highly indebted to bail out the banks again.

The only other alternative to an unbailed-out bank going spectacularly bankrupt, is what’s called a “bank bail-in”. This is where the bank who cannot con money from the government takes the cash from all the depositors and gives the savers a share of the bank itself.

This may sound reasonable, at first, until you realise that you cannot buy food or pay bills with bank stock. This means that many people will sell the bank stock and send the price plummeting. For an example, consider Deutsche Bank, whose stock price was almost $110 before the GFC, and now trades for under $7. This is one of the top twenty largest banks in the entire world, and their stock dropped by 95%.

The bank bail-in legislation has been passed by G20 nations, so it’s probably law where you are. Part of the explanation for having the bail-in provision is, (and I quote), “to reduce loss on bank shareholders, creditors and the Government.”

In simple terms, it’s a law to protect the government from having to go into further debt to bail out the banks for their irresponsible actions. In extended terms, it also says it is protecting the shareholders; because that’s what’s most important, right? ☹

Let’s be straight: I am not against shareholders or banks, or CEO’s, when they are doing the right thing. I do, however, have issue with any businesses who decide that taking care of themselves is far more important than taking care of their customers. This bail-in legislation enables sophisticated investors and bank shareholders to profit whilst ordinary account holders could potentially lose 99% of their cash, and it just plain stinks.

What do you do, to plan for #GFC2?

If the banks in the worldwide top 20 can go broke or drop 95%, then it is anyone’s guess which banks will be safe enough to hold your cash. We have already seen bank restructurings, massive layoffs and branch closures as banks react to a lower profit environment.

It’s possible that in a world where banks cannot be trusted, you should follow the advice of the great Jenny Morris and “trust yourself”.

Cryptocurrencies were created in part to deal with a world which is trustless; the perfect antidote for today’s banking and financial problems. Obviously, the price volatility in cryptos such as bitcoin mean that volatile crypto is not a perfect tool for managing day to day spending, so consider putting your spending cash into a stable coin in your local currency (TrustToken offers TrueUSD, TrueGBP, TrueAUD, TrueCAD, TrueHKD and more).

These stablecoins are almost always valued 1:1 for your local currency, and offer 99.99% stability. You can even use an “UNbank” such as Celsius to earn up to 8% interest on stablecoins, making it just like a traditional bank account (but with much better rates of interest).

BostonCoin has a varied basket of coins for both long and shorter-term holdings. We access additional earnings from using Celsius and we suggest anyone considering holding crypto for the longer-term should look at crypto bank services such as Celsius, MCO or other crypto lenders. As always, be sure to do your due diligence, check out the fine print and ensure your funds are safe and insured against loss.

How are we doing?

BostonCoin continues to monitor crypto markets as well as keeping an eye on the larger economic globe. Whilst we can have empathy for traditional bank savers who may lose again in #GFC2, and whilst we feel a level of righteous anger against pirate banksters and market manipulators, we accept the things we cannot change, and profit where we can.

This month we are barely paws*itive due to a big dive from most altcoins, lead by bitcoin, however, we hold out for better days coming soon and have faith in crypto as the world financiers seem to be getting lost in the woods.

Binance Coin still strong 136%

Snagride surging up 286%

ChainLink up 147%

Celsius up 139%

We added to our holdings in IOTA this month, taking advantage of the dips, and continue to look for good value.

BostonCoin NAV at 30/09/2019

22.5825

BOS price 24.8407

For those who may have opened a wallet in the heights of 2017 and forgotten how to use it, or for anyone wishing to learn more fundamentals of crypto investing, crypto wallet and exchange use, please drop us a line.

New Cryllionaire Crypto group chats will occur if demand is strong from you and your friends. Meanwhile, hang in there, add to your portfolio if you can during down times, and keep watching the horizon during choppy periods. We will get there 🙂

We will update the YouTube Channel with new interviews, and provide updates in Facebook group. Please contact us through Facebook if you have questions or comments.

Thanks for your continued suppawt…

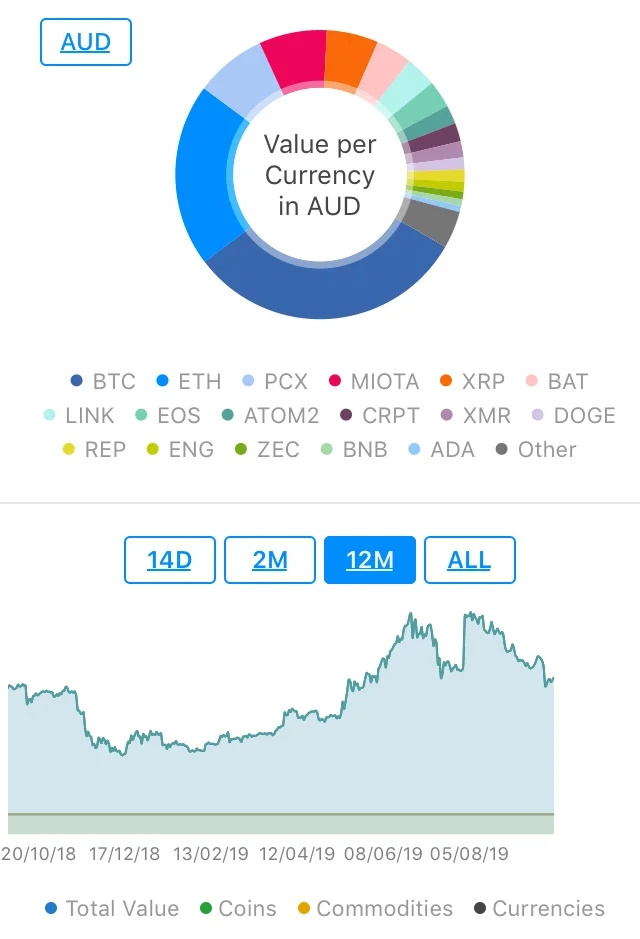

Performance of #BostonCoin portfolio over the last few months. Despite the dips, it’s a nice rise

NEWSFLASH:

Boston Trading Co. & Cryllionaire.com bring you a series of informative video interviews with the CEO’s of your favourite ICO’s. Search for #cryllionaire on Youtube or use this link.

We are committed to your crypto education. Tell your friends and score cool #BostonCoin promotional gear, as well as good karma.

You can share the posts from Youtube, Twitter or Facebook on your personal wall with one click, or compose your own post and use the hashtag #BostonCoin. Every month we will choose a winner and send you something cool from the #BostonCoin “swag bag” for sharing the love.

Share the love and score great prizes as well as good karma (or should that be #dogma?)

Copyright © 2019 *BostonTrading.co, All rights reserved.