What is risk and how do we manage it?

The fine-print on financial documents says “all investment involves risk”, but what exactly does that mean? Is it just the risk that your investment may go down? Are there different types of risk, and which ones do I need to know?

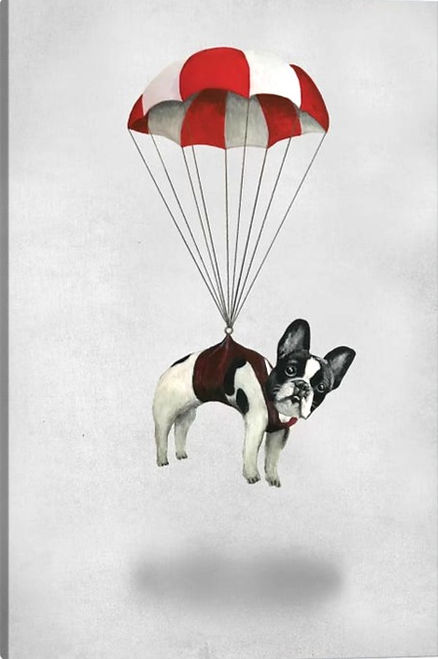

One of my favourite analogies for risk is a question, posed by a fund manager at a financial planning conference. He asked, “Two skydivers jump out of a plane. Person A is wearing a parachute; person B is not. Which person has the most risk?”

Please pause for a moment to answer the question in your own head before reading on for the answer.

What is risk?

Simply put, “risk” is the chance of something happening which you did not expect. In the above example, person B (wearing no parachute) could fully expect that they would descend quite rapidly and make a very sudden stop. There is no risk of any other outcome. The moment person B stepped out of the plane, their end result was a foregone conclusion.

Person A is actually the one who encounters risk. They have a parachute, and they expect to float gently down to earth. However, there is a tiny percentage risk that their parachute may malfunction, which could result in death.

It seems counterintuitive, as both skydivers were risking their lives; however one outcome was 100% certain, whilst one may have only been 99.99% certain. The remaining 0.01% was risk.

Types of risk

There are many types of risk (variations from an assumed outcome) in life. There are risks in driving a car, crossing the road, undergoing surgery, or even asking someone out on a date. Note well: The quality of your experience in life will be in direct proportion to your ability to understand and manage your risk.

Most people will look left and right (maybe twice) and then cross the road. Someone who is suffering from phobias or paranoia may become so terrified of crossing the road as to become housebound. Someone with no rationale may boldly walk across the road without looking, and will often become a statistic. Obviously, we wish to avoid the extremes of being too bold or too cautious, and live life happily with a modicum of risk and the appropriate reward.

Many of us have internal stories of times when we did not take a risk, and later regretted it. Most people have the “sliding doors” moment when they wonder, “What would have happened if I had told my high-school crush that I liked them? Would life have been better if I had taken that job? Where would I be now if I had bought that stock/land/crypto when I first heard of it, rather than a few years later?”

If you can understand that risk is not always sky-diving or life-threatening, then you can weigh up the pros and cons, and manage your risk appropriately.

If you confess your feelings to your crush and it is not reciprocated, it will not necessarily ruin your life, and there are plenty more fish in the sea. That dream job may or may not have worked out, but life goes on, and you will bounce back. Yes, we all wish that we had bought Bitcoin when it was under $3, but we cannot travel back in time, and in the next 10-15 years, you will probably be very happy that you got into the market when you did.

Investment risk

Most people think that investment risk is the risk that your investment will go down in value. This is true to a degree, however, there are other types of investment risk.

Market risk

Market risk is the risk that your investment may not perform as well as the rest of the market. It is entirely possible that your investment goes down, sure, that is mostly covered under investment risk. If instead, your investment goes up by 10%, and the rest of the market goes up by 40%, you have just encountered market risk.

The best way to manage this type of risk is to diversify into different types of investment. Every few years there will be a crash in stocks, crypto, bonds or property. The idea is that if your investments are in different areas, a big crash in one area wil be balanced out by good performances in other areas.

Remember, when one market “crashes”, the money is not lost. The money merely moves from one place to another. For example, in a stock market crash, a few billion dollars will seem to go missing from the stock market, but will show up in increased purchases of bonds or another asset.

Management risk

Management risk is a risk which lies directly with the person or persons who are managing the investment for you. You may find that a particular investment has been going well for five or six years, and then the management team changes, resulting in performance that is not necessarily in line with your expectations.

Sometimes this can be to the downside, where an investment that has been running at 10-15% per year can suddenly start running at 5-10% per year, resulting in some unhappy investors.

Sometimes the risk can be to the upside, where an investment has been running at 10-15% per year suddenly changes and starts making 50-60% per year. This outperformance sounds like a great problem to have, but some people may be upset to find themselves with an unexpected tax bill.

Capital risk

Capital risk is the risk of loss of part or all of your capital. A stock, crypto or bond may lose 100% of its value if the company goes bankrupt. Property may be more resilient, however, we have seen property prices crash by over 90% in some areas (eg. Zimbabwe after Mugabe’s dictatorship, Detroit USA, after the 2008 GFC, where houses once worth $750 000 could be bought for under $100).

Even keeping your funds in cash is no escape. Tales of hyperinflation in Zimbabwe, Germany and Venezuela are legendary, where wheelbarrows filled with billions in cash were needed to buy a loaf of bread.

Many people may be unaware of the life savings which were wiped out when one of Europe’s largest banks went bankrupt after the 2008 GFC, wiping out $10 billion worth of people’s deposits, and its stock dropping by 95%. Sometimes the adages “safe as houses”, “take it to the bank” and “cash is king” can be wrong.

While some bank deposits may be “guaranteed”, they are often only partially guaranteed, or backed by a government; which may default, settle for pennies in the dollar, or engage in quantitative easing (QE) to print more dollars, and further devalue your currency.

Again, the solution to capital risk is diversification. If you adore cash, you could limit your risk by having several deposits in different banks, or even different countries and currencies. If you love stocks, bonds or crypto, then aim to have a wide variety of investments, rather than putting all your eggs into the one basket.

Managing risk

There are no guarantees in life, and no matter how carefully you check the road before crossing, there is a tiny chance you can trip and fall, sneeze wrong and slip a disc or be struck by a meteorite.

As nobody can live a risk-free life or have a risk-free investment, the best we can do is to minimise known risks and use the tools we have at hand.

Managing risk with the “coin of coins”

Within the Bostoncoin portfolio, we manage known risks and diversify our holdings to limit downside and aim for upside. We also provide our coin selection methodology freely to anyone who wishes to learn, so that if one of our team goes down from accident or illness, someone else can step up to replace them.

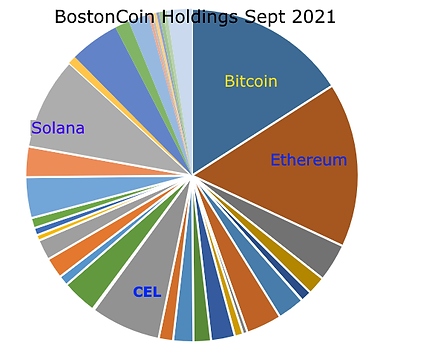

Below is a pie chart showing the Bostoncoin portfolio during September 2021. The top four holdings are labelled, and another 30+ holdings are not.

It makes sense for us to hold Bitcoin (BTC) and Ethereum (ETH), as these are among the oldest and most reliable cryptocurrencies, with their own blockchains. These OG (original gangster) cryptos could be compared to gold and silver, or Microsoft and Apple.

We also hold increasing amounts of the Celsius token (CEL), as this decentralised finance (DeFi) project continues to be a world leader in replacing traditional banks, with over one million unique customers and assets under management of over $24 Billion.

Solana (SOL) was a smaller project which we invested into as we believed it had strong growth potential, and may yet become a major competitor to Ethereum. We bought SOL when it was around $18, and watched as it soared all the way to over $200 within six months. Whilst we still believe the project is great and will have more growth potential, we sold out a portion of the SOL tokens at the high price, and retained around 80% of our initial SOL holdings.

Can any investment be risk-free?

The above SOL trade is one example of an almost risk-free trade: for example, if you can buy 100 tokens at $18 (total cost outlaid: $1800) and the tokens go up to $180 each (now worth $18 000), you can sell 10% of them and pay yourself back the original capital which you invested (10 x $180 =$1800 cash back).

You are now almost risk-free, as you can retain the leftover funds and know that, even if the tokens plummet to zero, you are not risking your own capital. You already have your original $1800 back in your pocket, and it is only the gain which is at risk; money which you never had in the beginning anyway.

We took the approach of “profit-taking” (selling off part of our holding for a large gain) and “rebalancing” (putting some of the profits back into some underperforming or cheaper tokens) so that our model portfolio does not become lopsided or have undue risk if one asset underperforms.

The Bostoncoin portfolio is now less risky (almost risk-free) with SOL, because if SOL goes to zero, we have our profits already, and if SOL continues to outperform, we still have a stake in that area.

Low risk vs No risk

We could also consider our Bitcoin holdings to be less risky (almost risk-free), as the government in El Salvador has recently declared Bitcoin to be a national currency. This means that millions of El Salvadorean citizens can be paid in Bitcoin, and spend Bitcoin at their local grocery store, coffee shop or burger joint. A currency supported by an entire country seldom disappears.

During the “flash crash” in late September when traders had fears of the Chinese Evergrande property fiasco, Bitcoin prices dropped briefly by up to 30%, but then prices recovered quickly as the El Salvador government swiftly jumped in to buy up more Bitcoin for its own currency reserves.

Knowing that at least one world government is out there to “buy the dips” may make many people feel more secure about investing into Bitcoin and other cryptocurrencies, which will lead to more price stability and faster recovery from any price falls.

If you had not seen the news about El Salvador, or if you are wondering which countries may be next to adopt Bitcoin as a national currency, feel free to watch “Bitcoin in El Salvador: Who’s Next?” a quick five minute appearance by the Bostoncoin CFO on national TV (thumbnail at bottom of the page).

We continue to monitor the markets: buying when our research suggests a coin is undervalued, and selling when we make massive gains or see a better opportunity. We also continue to add to our scrapbook of Bostoncoin in the Media, with an increasing number of articles across many areas and countries.

Winners this month include

Solana up 4 635% *

MATIC up 6 346%

AAVE up 59 402%

CAKE up 4 545% *

*Winners have figures annualised, from September 2020 to September 2021. You will notice that SOL is up 10 000%+ in the past six months, but annualised returns shown are lower, as they are averaged over a longer period. Some coins in the BostonCoin portfolio have been held for <6 months and some have been held for >2 years, but all returns are annualised for ease of comparison.

Bostoncoin is up 9.6% over last month and up 584.46% over the last year, outperforming Bitcoin yet again.

Meanwhile, the average managed fund in Australia has returned from 7.8% to 22.1% over the last twelve months, with some exceptional funds in the USA returning 14% up to 31% for the year. #justsayin’ #stickwiththepuppypack #tellyourfriends #Bostoncoin #coinofcoins #takethebiteoutofbitcoin

Once you understand risk, you can learn to manage or diminish your risks, and sometimes reduce them to very low, even if the risk is never actually zero. Now that you know how to reduce your risks in investments and in life, perhaps you may feel inspired to take other chances. Let your crush know how you feel, apply for that dream job, start a side-hustle business, or try a new hobby. #JustDoIt

at 24/9/2021

BOS NAV 215.436764

BOS Price 236.980441

MOM up 9.6%

YOY up 584.46%